meLOC (Home Equity Line of Credit)

A new home equity line that’s all about you.

meLOC: The flexible new HELOC that locks rates right where you need them.

Your home is a reflection of you, so why shouldn’t your loan be also? Whether you dream of an epic vacation, college degree, home renovation or more – our powerful new equity line gives you the freedom to lock rates whenever you want and keep that rate until the balance is paid. With a low rate that’s there when you need it, you can relax and enjoy the comfort of this sweet home equity loan.

Make your home equity work harder and smarter.

Between bucket list dreams and to-do list projects, you have exciting choices to make. Fortera’s meLOC lets you focus on these instead of deciding between the locked rate of a home equity loan or the flexibility of a line of credit. meLOC gives you both. It’s our Home Equity Line of Credit (HELOC) that’s ready when you are and offers you the advantage of locking in fixed lower rates until the balance is paid.

How does a Home Equity Line of Credit Work?

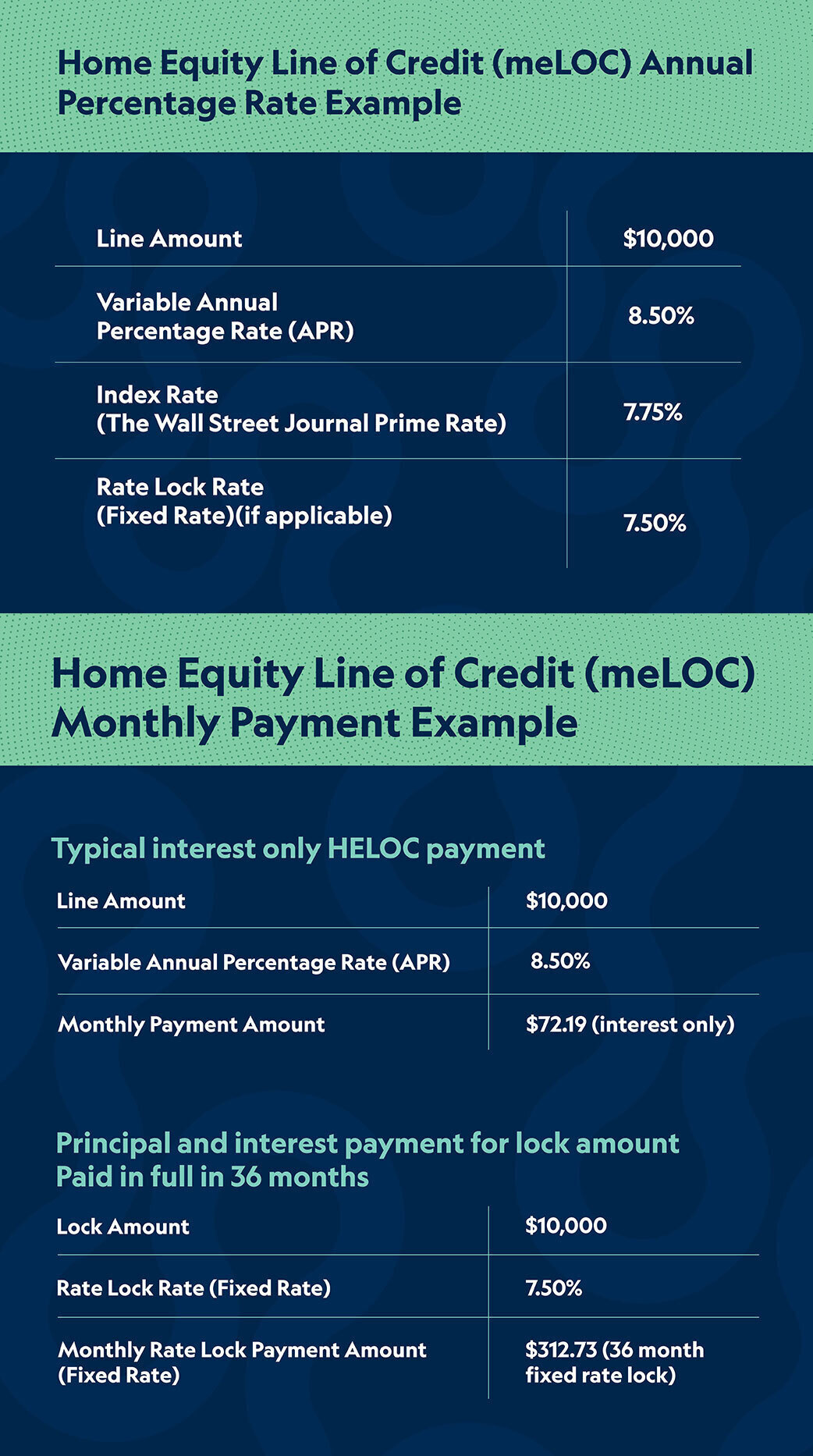

A Home Equity Line of Credit provides funds for you to balance larger expenses with big time flexibility. Once approved, you have full access to your funds at the ready. You can make withdrawals up to your approved limit whenever you would like (certain fees may apply) and our meLoc even lets you check off multiple items on those bucket and to-do lists together. You’ll have the ability to use up to three rate locks* at one-time. Each lock will have its own rate that is locked in for up to a 10-year term. Once you’ve paid off one of the locks, you can add another in its place.

Take advantage of interest rate changes with a variable APR* starting at 8.50%1 or 9.00%2.

Stages of a HELOC:

- Draw Period: (the first 10 years) Use your line of credit while making interest-only payments with the option to pay extra against the principal.

- Optional Rate Lock: for up to three portions of your balance, you can lock the rate and start making payments. NOTE: Locks are subject to fixed rate pricing which may be lower than your current variable rate.

- Repayment Period: (the last 20 years), make monthly principal and interest payments to repay the outstanding balance. Note that you won’t be able to draw funds or exercise rate locks from the HELOC during this time.

meLOC (Home Equity Line of Credit) Rates

| Type | Term | APR* |

|---|---|---|

Type:

Interest Only Payment | Loan to value is less than 80%

| Term:

N/A

| APR*:

8.50%- 11.00%**

|

Type:

Interest Only Payment | Loan to value is greater than 80%

| Term:

N/A

| APR*:

9.00%- 9.50%**

|

meLOC's adjust monthly on the first day of the month. There is no limit on the amount by which the annual percentage rate can change during any one-year period. The maximum rate is 18.00%. The minimum rate will never be below 3.25%. *APR=Annual Percentage Rate. The ANNUAL PERCENTAGE RATE you receive will be based on credit worthiness and loan to value amount. Not all members will qualify for the best or lowest rate. All loans are subject to approval. Rates, terms, and conditions are subject to change.

Auto-pay Advantage: A discount of 0.25% will be deducted from the above stated annual percentage rates when the payment is received automatically from a Fortera draft account. This discount is only available on new loan transactions with an effective date on or after the date of this addendum. The annual percentage rate will default back to the normal rate in the event the payment status or draft account status changes.

**Loan to Value Ratio (LTV): A ratio used by lenders to calculate the loan amount requested as a percentage of the value of a home. To determine the loan to value ratio, divide the loan amount by the home's value. The LTV ratio is used to determine what loan types the borrower qualifies for as well as the cost and fees associated with obtaining the loan.

1Interest only Payment Loan to value is less than 80% (9.00%-11.50%APR). 2 Interest Only Payment Loan to Value is greater than 80% (9.50%-10.00%APR) HELOC's adjust monthly on the first day of the month. There is no limit on the amount by which the annual percentage rate can change during any one-year period. The maximum rate is 18.00%. The minimum rate will never be below 3.25%. *APR=Annual Percentage Rate. The ANNUAL PERCENTAGE RATE you receive will be based on credit worthiness and loan to value amount. Not all members will qualify for the best or lowest rate. All loans are subject to approval. Rates, terms, and conditions are subject to change.

Auto-pay Advantage: A discount of 0.25% will be deducted from the above stated annual percentage rates when the payment is received automatically from a Fortera draft account. This discount is only available on new loan transactions with an effective date on or after the date of this addendum. The annual percentage rate will default back to the normal rate in the event the payment status or draft account status changes.

**Loan to Value Ratio (LTV): A ratio used by lenders to calculate the loan amount requested as a percentage of the value of a home. To determine the loan to value ratio, divide the loan amount by the home's value. The LTV ratio is used to determine what loan types the borrower qualifies for as well as the cost and fees associated with obtaining the loan.

Home Equity Line Of Credit Benefits

Apply now

Apply for a meLOC today. With no application fee, what are you waiting for?

Helpful Resources

More tools and services to make your day a little easier.

Submit a Debt Protection Claim

Need to submit a claim? No problem, we've got you covered. You can submit a claim at myclaim.cunamutual.com. If you have any questions, please text us at 931.431.6800 or email us at info@forteracu.com and we will be happy to help.

Document Checklist for Home Equity Line of Credit Applications

To verify your identity, we always ask that you come prepared with a government-issued ID. It is important that it is not expired. Examples of acceptable IDs include a State Driver's License or a U.S or Foreign Passport. If we have trouble validating your ID, we may ask for a secondary ID. If you have a question about whether or not an ID can be used, just text us at 931.431.6800.

In addition to identification, you will also need to bring:

- A copy of your homeowner's insurance (the declaration page)

- A copy of your recorded deed

- A home assessment or appraisal

- Your income verification

- Copies of billing statements with full account numbers and payment addresses (this only applies to debt consolidation)

- A 10-Day payoff quote (this only applies to debt consolidation)

If you have any questions about this list, please email us and we will be happy to help.

Learn About Additional Insurance Coverage With TruStage

As a Fortera Credit Union member, you have access to additional insurance protection through our partner, TruStage. They provide Life, Auto, Home, and Accidental Death Coverage. You can get up to $1,000 of Accidental Death coverage for free by visiting trustage.com and claiming your offer.

If you have questions for our team about TruStage insurance, please text us at 931.431.6800 or email us at info@forteracu.com.

Add Debt Protection to Your Loan

If your life takes an unexpected turn, your family’s finances can be strained. But with Member's Choice Borrower Security with Life Plus, your loan payments or balance may be canceled, up to the contract maximums, in case of involuntary unemployment, disability, or death. It’s just one more way you can look out for the people you love.

Take an important step toward financial security. Email us at loans@forteracu.com and ask about Member's Choice Borrower Security with Life Plus today.

Your purchase of Member's Choice Borrower Security with Life Plus is optional and will not affect your application for credit or the terms of any credit agreement required to obtain a loan. Certain eligibility requirements, conditions and exclusions may apply. Please contact your loan representative or refer to the Member Agreement for a full explanation of the terms of Member's Choice Borrower Security with Life Plus. You may cancel the protection at any time. If you cancel protection within 30 days, you will receive a full refund of any fee paid.

Unique ID & Copyright

DP-3415592.1-0121-0423 CUNA Mutual Group ©2023, All Rights Reserved.

Need a hand?

Tag us in. Whether you are on your couch or halfway around the world, use Fortera Video Chat to get quick answers from a friendly face.

What is a home equity line of credit?

A HELOC or home equity line of credit (we call ours meLOC), makes a specific amount of money available to you for a set period or term. During the term, you can advance – or draw – the funds, as needed. When you reach the end of the draw period, you can no longer access additional funds and need to start repaying what you borrowed plus interest.

During the draw period, you may have only made minimum monthly payments (which may have been interest only). When the repayment period begins, you'll need to make principal and interest payments to repay your principal balance within a specific time frame.

What is the difference between a Home Equity Loan and a Home Equity Line of Credit?

The two biggest differences between a Home Equity Loan and a Home Equity Line of Credit are the types of interest rates for each loan and how one receives their funds. Home Equity Loans are fixed-rate loans and they are given to the member in one large lump sum. Home Equity Lines of Credit are variable rate loans and members receive access to a line of credit. They can borrow as much as they need without having to commit to a large lump sum.

How is a Home Equity Line of Credit different from a Credit Card?

These financial tools are very similar. The largest difference between the two is how they are accessed. Credit Cards are loans designed to be convenient for our members. Need a mini loan? Grab your credit card and get what you need. Because HELOCs do not come with a card, spending money does not usually happen instantly. For many of our members that do not feel comfortable with a Credit Card or struggle with overspending or splurge-spending, a HELOC can be a great tool because it requires you to slow down and think before making a large purchase.

How do I know the type of home equity financing I have and which repayment plan I have?

You can speak with one of our Loan Servicing Specialists to get this information. You can reach them by calling 931-431-6800 ext. 8217. They can provide information about what type of home equity loan you have and your repayment options.

What would I use a Home Equity Line of Credit for?

This loan is great for projects that don't have a fixed price. If you are remodeling your kitchen, adding a deck to your home, paying for some additional college courses, etc. this is a great option for you. It allows you the flexibility to borrow what you need instead of requiring you to borrow a larger sum.

Why do principal and interest payments matter?

If you've been making mostly interest-only payments and not many principal payments, you have not been reducing the amount you owe. The principal-plus-interest payment is typically much higher than an interest-only payment.

What does end-of-draw period mean and what happens?

For a home equity line of credit, the end-of-draw period is the point at which you can no longer access funds. Most lines of credit have a draw period and then move into the repayment period, when you'll repay your outstanding balance with full principal and interest payments.

For example, on a $50,000 outstanding balance, the interest-only payment at 8.50% would be roughly $212 monthly, while the principal and interest payment at the adjusted rate of 8.50% would be roughly $437. (Based on a 20-year-repayment plan – referred to as the amortization period.)

How far in advance should I prepare for the end of access to the funds, or the end of my loan term?

The sooner you start making principal and interest payments, the better, because it will help you when your account enters the repayment period. Pay particularly close attention to your home equity account at least one year before it enters the end-of-draw period.

Can I renew or refinance my home equity line of credit or loan?

In some situations, you may be able to refinance or renew the home equity line of credit to change the limit amount or account type. You can contact the lending center and speak with a loan agent at 931-431-6800 ext. 2258, to discuss which option may work best for you.

Can I get an extension on my current draw period date?

In some situations, you may be able to refinance or renew the home equity line of credit to change the limit amount or account type. You can contact the lending center and speak with a loan agent at 931-431-6800 ext. 2258, to discuss which option may work best for you.

What happens if I can't refinance my outstanding balance?

The current balance will go in to the contract repayment terms.

What if I don't have any equity in my home?

We may have options for home equity members who are approaching the end-of-draw period and have little or no equity in their homes. To learn more, call our lending center to speak with a loan agent at 931-431-6800 ext. 2258.

Can I pay my home equity line of credit in full?

Yes, you can. To find out your payoff amount, call us at 931-431-6800 ext. 8217.

What documents do I need to apply for a Home Equity Line of Credit?

To verify your identity, we always ask that you come prepared with a government issued ID. It is important that it is not expired. Examples of acceptable IDs include a State Driver's License or a U.S or Foreign Passport. If we have trouble validating your ID, we may ask for a secondary ID. If you have a question about whether or not an ID can be used, just text us at 931.431.6800.

In addition to identification, you will also need to bring:

- A copy of your homeowners insurance (the declaration page)

- A copy of your recorded deed

- A home assessment or appraisal

- Your income verification

- Copies of billing statements with full account numbers and payment addresses (this only applies to debt consolidation)

- A 10-Day payoff quote (this only applies to debt consolidation)

What's New